New Jersey online casinos haven’t shown a lot of revenue growth so far in 2024.

The NJ Division of Gaming Enforcement (DGE) released the figures for July earlier this week. Online casino gaming brought in $134.4 million in gross gaming revenue (GGR), while online poker rooms contributed another $2.3 million, for an iGaming total of $137.7 million.

That’s a small increase from $130.9 million in June. However, June is also one day shorter than July. To assess growth rates, it’s better to look at daily average gross gaming revenue (DAGGR). Using that metric, revenue actually slowed from June to July, albeit by a mere 0.6%. It has also remained almost unchanged since January.

Summer is always a little slower for online casinos. Nice weather means there’s more competition from non-gambling activities for people’s time and spending money. There’s also less crossover from mobile sportsbooks since there’s less to bet on while the NBA and NFL are on hiatus.

Even so, this is a particularly slow summer. Year-over-year growth stats demonstrate this, providing an apples-to-apples comparison that removes seasonality from the equation.

To start 2024, online casinos and poker were showing 33% annual growth, similar to the average pre-pandemic rate of 35% from 2016 through 2019. That has dropped to just over 15% in July, the slowest rate seen since June 2018.

Online casinos everywhere got a huge boost when retail casinos shut down during the first year of the pandemic. There was no sudden drop in online revenue as restrictions eased. Slower growth now may simply be a more gradual, long-term correction for that boom period.

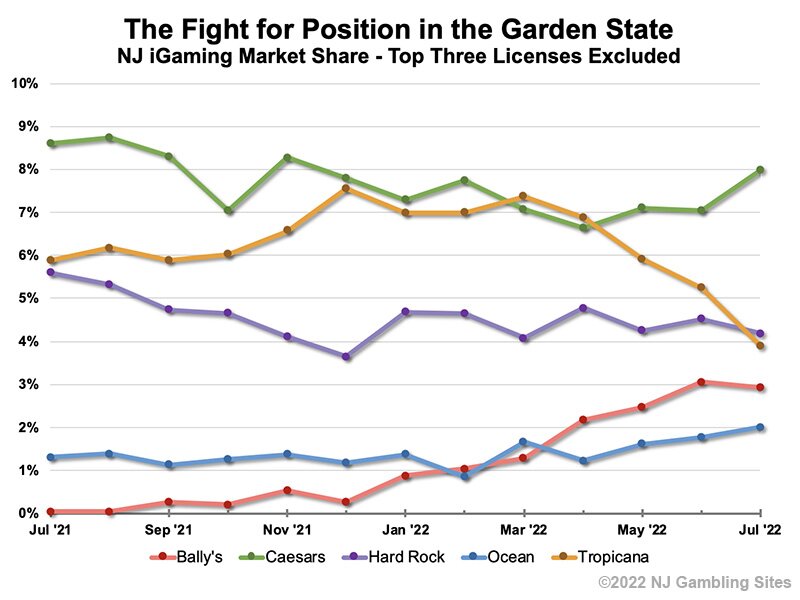

Rapid Movement Among Smaller Licenses

Though the total NJ market may be going through a slow period, there’s been plenty of activity in the race for market share.

That’s especially true for the smaller licenses. The big three – Borgata, Golden Nugget and Resorts – hold a combined 79% of the market. That total is virtually unchanged since last year, though Golden Nugget has been gradually slipping and Resorts gaining.

Let’s look at who’s winning and who’s losing among the other 21%.

Bally’s is an obvious license to look at, having been effectively nonexistent until this year. Through H1, it gained steadily, but in July it has shown its first indication of leveling off. If it stays where it is, it will hold 3% of the market, putting it in between Ocean and Hard Rock.

Competition between those two licenses has also gotten tighter. Ocean has traditionally been the smallest in the market, but has nearly doubled its share over the past year, hitting 2% for the first time in July. Conversely, Hard Rock has been on the decline, having lost 1.4 percentage points over the past year.

Caesars had also been losing market share, and temporarily lost its fourth-place position in March and April. However, its DAGGR bounced back nearly 13% in July, so it may have turned the corner.

Tropicana grew strongly through H2 2021, but has taken a plunge in recent months. This is because it has had to shut down its flagship skin temporarily while changing software suppliers. Tropicana revenue should rebound at least partially once it finishes the transition and relaunches its namesake site.

It might not make it all the way back to its former levels, however. Another former Tropicana skin, Virgin Online Casino, has migrated to the Bally’s license, also for supplier-related reasons.

About the Author